Last Updated on February 28, 2026 by Matthew Hallock

The VGS Chain: How the State’s Outsourced Valuation System Preceded a $20,000 Drop in Joseph Ganim’s Property Tax Bill

The disparity in Connecticut’s property assessment system has been underscored by recent records in Bridgeport, where Mayor Joseph Ganim’s real estate transactions and subsequent property tax reductions have drawn public scrutiny. While many residents face increasing annual property tax burdens, municipal records reveal a different trajectory for the city’s chief executive. At the center of the inquiry is Ganim’s 2021 acquisition of a Black Rock neighborhood property—a transaction that included a separate, developable lot for no additional recorded cost and was followed by a substantial reduction in the property’s assessed value. The circumstances surrounding this multi-layered transaction highlight broader questions regarding transparency and the internal mechanics of the municipal assessment process.

The assessment of property values across Connecticut is a complex process, largely navigated through third-party firms. In Fairfield County, many municipalities, including Bridgeport, contract with Vision Government Solutions (VGS) to perform these valuations. This model creates a multi-layered chain: the municipal assessor’s office hires a primary firm (VGS), which may then utilize subcontractors, such as Tyler Technologies, for physical valuation work. Analysts of this structure argue it can dilute direct accountability between the local assessor’s office and the contracted firms.

This lack of direct oversight is often compounded by a lack of physical rigor; in many jurisdictions, actual interior inspections of properties are rare. Data suggests that only a small fraction—estimated at 5-10%—of homes are inspected firsthand, leaving the majority of valuations to be determined by exterior observations and algorithmic models. This reliance on remote data contributes to volatility in property taxes and creates the potential for significant valuation discrepancies, as seen in the Bridgeport case.

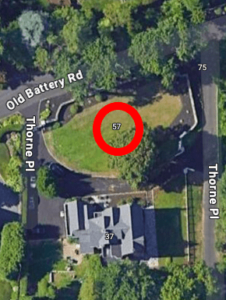

The transaction focuses on 37 Thorne Place in the Black Rock neighborhood, the location Mayor Ganim declared as his residence in mayoral campaign filings despite the property’s subsequent sale in May 2023. Ganim purchased the residence in 2021 for $333,000, a figure notably below its market list price of $699,900. Official Bridgeport property records—specifically the field cards—further complicate the timeline, showing a purchase price of $0 for this and several prior transactions. This documented omission in city records remains an unaddressed technical irregularity in the narrative of the property’s history.

Bird’s eye view of 37 and 57 Thorne Place, Black Rock, Bridgeport, CT

Further inquiry is directed at the inclusion of a separate parcel in the 2021 deal. The land, a .28-acre lot labeled 57 Thorne Place, was bundled into the transaction for a recorded price of $0. Despite its potential as a developable site, it was assessed at $16,530, which increased in 2025 to $23,980.

Following the 2021 purchase, the property at 37 Thorne Place received a tax reduction that lowered the annual payment from approximately $30,000 to roughly $10,000—a 66% decrease. This adjustment followed what is categorized as an “informal assessment.” Public transparency regarding this change is limited; the Board of Assessment Appeals spreadsheet does not list the address alongside other tax adjustments. Additionally, the 2024 property card currently on file omits data from previous years that would document the specific assessment cut.

Ganim eventually sold the house and the vacant parcel in May 2023 for a combined total of $1.1 million. The intersection of the initial purchase price, the subsequent tax reduction, and the eventual profit realized upon sale continues to serve as a primary case study for those questioning the equity of Connecticut’s municipal assessment framework.